- Cover up to 100% of the cost of attendance1

- For students in associates, bachelors, and graduate programs at select colleges and universities

Here’s our current career loan interest rates:

Variable rates

3.89%

to 17.99% APR

Fixed rates

2.39%

to 17.99% APR

(all rates shown include auto-pay discount)2

Get Started with the Right Loan for Your Career

Variable and Fixed Rates: Which is right for you?

It’s important to understand the difference between variable and fixed interest rates2 on student loans. Learn the basics so you can pick the best one for you with confidence.

Variable Rate

3.89%

to 17.99% APR

*all rates shown include auto-pay discount2

Variable interest rates can change during the life of the loan. They are based on a publicly available interest rate index that changes in each month. Changes in the index will change your monthly payment amount.

Changes to the rate are typically based on a publicly available interest rate index such as the prime rate or SOFR.

Fixed Rate

2.39%

to 17.99% APR

*all rates shown include auto-pay discount2

Fixed interest rates stay the same for the entire repayment period. You will have the same monthly payment amount every month after entering full repayment.

Cosigning Made Easy

Usually, students don't have the credit or income requirements to qualify for a student loan by themselves.

A parent or other adult with good credit will need to cosign the private student loan.

Both the student and cosigner share equal responsibility for the loan.

0%

of all undergraduate loans are cosigned

0%

of borrowers choose an in school repayment option

How Do We Compare to Other Private Lenders?

| College Ave | Sallie Mae | Citizens Bank | |

|---|---|---|---|

| Number of Repayment Options |

4 |

3 | 3 |

| Select Your Own Repayment Term |

|

Limited | Limited |

| Apply in as Little as 3 Minutes |

|

|

|

| No Application or Origination Fees |

|

|

|

*Comparisons based on information obtained on lenders’ websites as of February 24th, 2026.

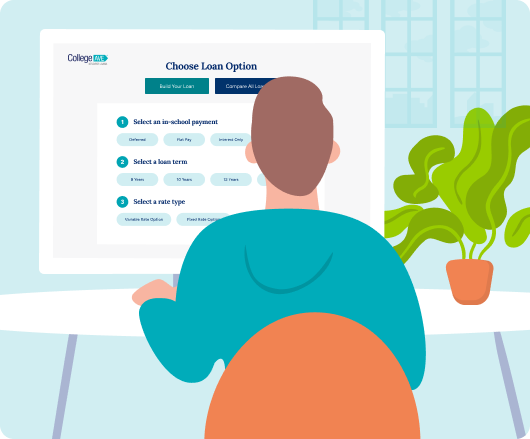

See Your Career Loan in Action

Put anxiety on the sideline when you see what your future loan will look like and how you can make your loan work for you. We’ll show you all your options and rates so there are no unexpected surprises.

0%

of our undergraduate borrowers are approved for additional loans

Don’t worry, we’ve got a better student loan process

1

Before school starts, figure out how much you’ll need to borrow. A good estimate is to take your cost of attendance and subtract any scholarships, grants, federal loans in the student’s name, and savings you plan to use.

2

Start shopping around for loans and apply for a student loan about 30 days before classes start. Know who your cosigner is and choose your loan term and repayment options.

3

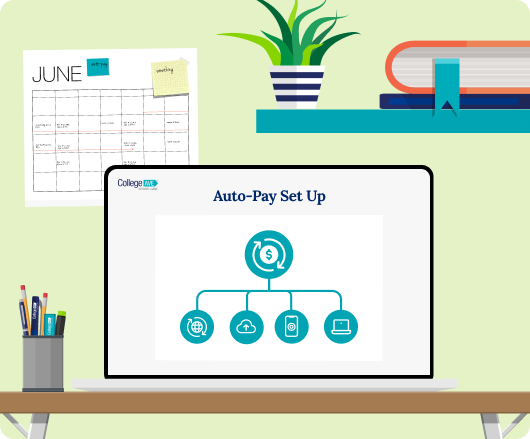

Once approved, we’ll work directly with your school to certify the loan. After the money is sent to your school, be on the lookout for your first loan statement. If you selected an in-school repayment option, consider signing up for auto-pay.

Apply Now for a Loan Check Application Status 1

Before school starts, figure out how much you’ll need to borrow. A good estimate is to take your cost of attendance and subtract any scholarships, grants, federal loans in the student’s name, and savings you plan to use.

2

Start shopping around for loans and apply for a student loan about 30 days before classes start. Know who your cosigner is and choose your loan term and repayment options.

3

Once approved, we’ll work directly with your school to certify the loan. After the money is sent to your school, be on the lookout for your first loan statement. If you selected an in-school repayment option, consider signing up for auto-pay.

Apply Now for a Loan Check Application StatusFootnotes

1

As certified by your school and less any other financial aid you might receive. Minimum $1,000.

2

Variable rates may increase after consummation. The 0.25% auto-pay interest rate reduction applies as long as a valid bank account is designated for required monthly payments. If a payment is returned, you will lose this benefit. Approved interest rate will depend on creditworthiness of the applicant(s), lowest advertised rates only available to the most creditworthy applicants and require selection of the Flat Repayment Option with the shortest available loan term.

3

This informational repayment example uses typical loan terms for a freshman borrower who selects the Flat Repayment Option with an 8-year repayment term, has a $10,000 loan that is disbursed in one disbursement and a 7.78% fixed Annual Percentage Rate ("APR"): 54 monthly payments of $25 while in school, followed by 96 monthly payments of $176.21 while in the repayment period, for a total amount of payments of $18,266.38. Loans will never have a full principal and interest monthly payment of less than $50. Your actual rates and repayment terms may vary.

4

This informational repayment example uses typical loan terms for a freshman borrower who selects the Deferred Repayment Option with an 8-year repayment term, has a $10,000 loan that is disbursed in one disbursement and a 7% variable Annual Percentage Rate (“APR”): 96 monthly payments of $179.28 while in the repayment period, for a total amount of payments of $17,211.20. Loans will never have a full principal and interest monthly payment of less than $50. Your actual rates and repayment terms may vary.