For many high school students, undergrads, and parents, a college degree will affect your finances for the next five, ten, or even twenty years. The average college student at a private institution pays more than $35,000 in yearly tuition—that’s more than $140,000 over the course of a four-year degree. (US News) Since most undergrads and their families don’t have that kind of money available through savings and income, they turn to student loans to help pay for school.

No matter whether private or federal, when you’re applying for student loans, knowing how to compare student loan options like repayment terms and interest rate types while shopping can make the process a lot easier. In fact, the loan options you choose can end up saving you thousands of dollars in the long run.

But scrolling through hundreds of student loan options is a huge task. If you don’t understand all the factors that go into the final calculation, you’ll end up comparing apples to oranges and paying more than you need to.

The list below outlines the most important factors you should consider when comparing student loan costs and how each one affects the total amount you’ll pay in the end.

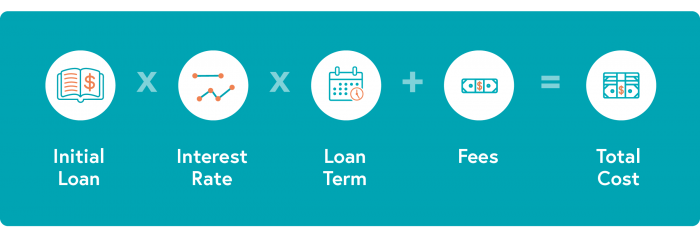

Basic Student Loan Math

Loan Amount * Interest * Term + Fees = Total Loan Cost

Types of Student Loan Options

In the simplest terms, a loan is borrowed money that must be paid back with interest. They are different from other types of financial aid such as scholarships and grants, which do not need to be repaid. Loan types vary according to the lender, their terms, and the associated costs. The government funds federal loans and private loans are funded by private lenders like banks and financial companies.

Federal Student Loans

The following are types of federal student loans.

- Direct Subsidized Loans (subsidized Stafford loans)

- Direct Unsubsidized Loans (unsubsidized Stafford loans)

- Perkins Loans

- Direct PLUS Loans

Private Student Loans

Private student loans for undergraduate students function similarly to other types of private loans like car loans or mortgages, since they require credit and income review of you or a cosigner. Private lenders can be any non-government organization, like a bank, credit union, state agency, or a school. Private student loans might offer lower interest rates depending on your credit.

These are the broad categories of student loan types. For a more in-depth analysis, check out this article that compares federal vs. private loans.

Student Loan Costs

Don’t skip the research phase when considering your student loan options. From your initial loan amount to interest rates and how long it takes you to repay, there are five key variables that you’ll need to compare when choosing a student loan:

- Interest Rates: Accruing annual percentage of the total loan amount you must pay while the loan is outstanding

- Fees: Varying costs for taking out a loan such as application or origination fees

- Monthly Payments: Agreed minimum amount you pay toward your loan each month

- Loan Term: The amount of time it’ll take you to repay the loan once the loan enters repayment

- Final Cost: The total amount you end up paying for your loan including interest and fees

Interest Rate

Every student loan charges interest, which is essentially the cost of borrowing money. Interest rates are part of how lending organizations charge for the services they provide. The interest rate is a percentage of the total loan amount that accrues daily, adding to the total amount you’ll need to pay back. These rates vary across lenders and can even shift depending on the length of your loan. If you’re taking out a private loan, your credit score (or your cosigner’s credit score) and income may also affect your rate.

Interest rates are important because they affect the total cost of your loan. For example, if you take out a five-year $10,000 loan with 0% interest, you’ll owe $10,000 at the end of those five years. But if you have a fixed interest rate of about 10%, you’ll owe almost $20,000 at the end of those five years.

That’s why shopping for a low rate is important—no one wants to pay more than they have to. Even a few percentage points can bump up your loan amount substantially. Use a student loan calculator to estimate how much the interest rate will increase your final loan amount. Keep in mind, the quicker you pay back a loan, the less you’ll pay in interest.

But remember that the rate isn’t the only factor that affects the total cost of your loan or monthly payments. When thinking about interest rates, you’ll also want to carefully consider whether you’d prefer a fixed interest rate or a variable interest rate.

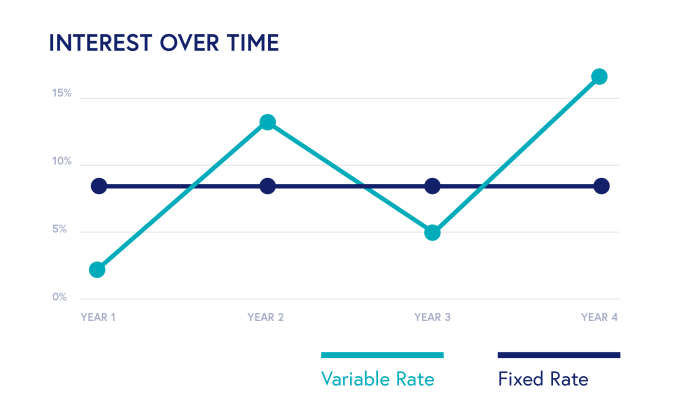

Fixed vs. Variable Interest Rates

Fixed interest rates won’t go up or down while you’re repaying your loan, so your monthly payments (interest + principal amount) will stay the same. A variable interest rate can fluctuate with the market and change your minimum monthly payments over time. When you’re taking out a student loan, the starting variable rate will usually be lower than the offered fixed rate but has the possibility of going up or down over time. Some people prefer the fixed rate, which adds the security of knowing that their monthly payment will always be the same.

Federal student loans only offer fixed rates, whereas private lenders typically offer both fixed and variable rates. In either case, you should carefully consider whether you prefer a fixed or variable rate and choose the interest type that works for you and your budget.

Fees

In addition to interest rates, some lenders may also charge loan origination fees. These are one-time fees that are paid upfront when the loan is first taken out, and they’re usually a percentage of the amount you borrow.

Federal student loan origination fees typically range anywhere from 1.068% to 4.276% of the total loan amount, depending on the specific type of federal loan. Many private student loans, like the ones we offer at College Ave, don’t have origination fees. When shopping around for other loans, make sure you know exactly what fees you’re expected to pay and when.

Loan Term and Monthly Payments

Your loan term is how many months or years it will take you to pay off your loan by making the minimum monthly payments. Before committing to a loan, you should calculate and understand what your monthly payments will be. While lower monthly payments might be more feasible, choosing a longer term will increase the total cost of the loan. Use a calculator to compare interest rates and payment terms for the loans you are considering.

A popular rule of thumb: You shouldn’t borrow more for school than you expect to earn your first year out of college. Research your possible career path to get an idea of the typical starting salaries for new graduates in your field. If you’re not sure exactly what path you’ll take, compare a few of the most likely options and plan for the scenario that pays the least. One of the easiest ways to get an idea of monthly payments is to talk to friends, family, and advisors who have been there. They can help you set realistic expectations for what you’ll earn, common living costs, and how to budget for life after graduation.

Overall, you need to find the perfect balance between an affordable monthly payment and a shorter loan term, so you pay the least amount of interest. That’s why it’s smart to have an idea of what you’ll be able to afford now, when you graduate, and ten or twenty years down the line.

Total Cost

Your monthly payment is equally as important as the total cost of your loan over the years. These are two factors you must compare for all the loans you research. The quickest way to determine the total cost of your loans is to use a tool like the College Ave Undergraduate Student Loan Calculator. Having multiple repayment options can help you find ways to reduce your loan amount, extend your term, or get the lowest possible interest rate. We know understanding loan calculations is difficult, but don’t let that stop you from comparing all your options.

Reviews

Beyond the terms of the loan, make sure you’re comfortable with the lender and its reputation. What are customers saying? Read their reviews, verify the lender’s Better Business Bureau rating, and check with people you know to find out what experiences they’ve had (good and bad) with lenders.

College Ave Student Loans offers student loan options that serve different students’ financial needs, including undergraduate student loans and graduate student loans. We also offer loans exclusively for parents who want to pay for their child’s college expenses. Learn more about the different student loans available, and what our customers have to say about us.