If you’re in college or have already graduated, it’s completely normal to be researching how best to deal with your student loans. Many people look for ways to lower their interest rate or monthly payment to make the loan more manageable over time. That’s one of the biggest benefits of refinancing. Student loan refinancing options let you establish new terms for your loan so you can breathe easier.

Here are five tips for refinancing your student loans:

1. Know the Difference Between Student Loan Refinancing and Consolidation

Many people don’t know the difference between student loan refinancing and consolidation. Both options let you combine your existing student loans into one loan, requiring just one monthly payment instead of multiple spread across different loans or lenders. Consolidation is reserved for federal student loans only under the Direct Consolidation Loan program. It’s a good choice if you have federal loans you want to combine without forfeiting benefits like loan forgiveness and flexible payments.

Refinancing is for any combination of private and federal loans. If you have multiple private student loans and want to combine them into one, refinancing may be right for you. Most people choose to refinance student loans because it allows you to change the terms that you originally agreed to when taking out each loan. Your improved credit score and higher income may help you qualify for a lower interest rate or more affordable lower monthly payments.

Do you have more consolidation questions? Check out Should I Consolidate My Student Loan or Refinance?

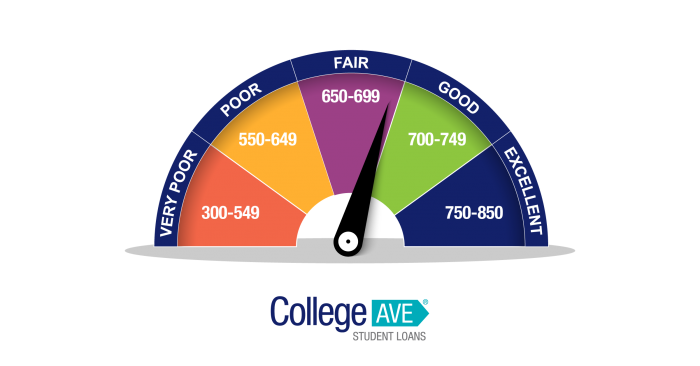

2. Know Your Credit Score

Your credit score is a major component in the student loan refinancing game. There are many online resources that will let you check your credit score for free. Take advantage of these services to get a better idea of what type of refinancing terms you could qualify for. All private student loans require a credit and income review. Knowing your credit score can help you understand what kind of loan and interest rates you may qualify for.

3. Get a Cosigner

If you find that your credit score is too low and you don’t qualify for a refinance loan on your own, then you’ll need to find a cosigner. A cosigner is someone who will take out the loan with you, guaranteeing to the lender that it will be paid back in full, on time. The cosigner shares equal responsibility for the loan. If you don’t make the monthly payment on the loan, then the cosigner is responsible for that payment. Cosigners provide added insurance through good credit, steady income, and a demonstrated ability to repay the loan if you are unable to.

If you believe your cosigner has all the prerequisites for the loan, invite them to use our free pre-qualification tool to get an idea before they apply if their credit score meets our requirements.

4. Calculate Your Debt-to-Income Ratio

When you research student loan refinancing options, you’ll find that many private lenders are interested in your current debt-to-income ratio. That ratio represents how much of your income is going directly to paying off any debt obligations. Calculate your debt-to-income ratio by dividing your monthly debt payments (including student loans, credit card payments, mortgages, car payments, etc.) by your gross monthly income.

The lower that percentage, the more likely lenders will be to give you better loan terms. They’re looking for assurance that you’re fit to repay the loan and on time. If you find that your ratio is high, then it’s time to figure out ways to either increase your income or decrease your debt. Remember that small steps make a big difference, like trading in for a car you can pay off or reducing credit card spending as much as possible.

5. Get Pre-Qualified

The easiest way to start the process of refinancing your student loans is to use prequalification tools to see if you qualify and what rates you can expect for student loan refinancing. You can use our pre-qualification tool to get your results. At College Ave we also offer a refinance loan calculator that will show you how much money you can save by refinancing your loans—from undergrad and grad to medical and dental. You can enter your credit score and your preferred loan term, and interest rate type (variable or fixed) and it will calculate your estimated new cost and monthly payment.