Managing your own money is hard — there are so many demands on your budget: rent, student loan payments, car insurance, groceries, and more. And with rising prices, it’s no wonder that many people feel like they are barely scraping by.

According to a recent study from the Financial Industry Regulatory Authority (FINRA), 51% of adults said they spend more than they make each month or make just enough to cover their expenses. If you are living paycheck to paycheck or relying on credit cards to make up the shortfall, creating a budget is key to getting your finances on track.

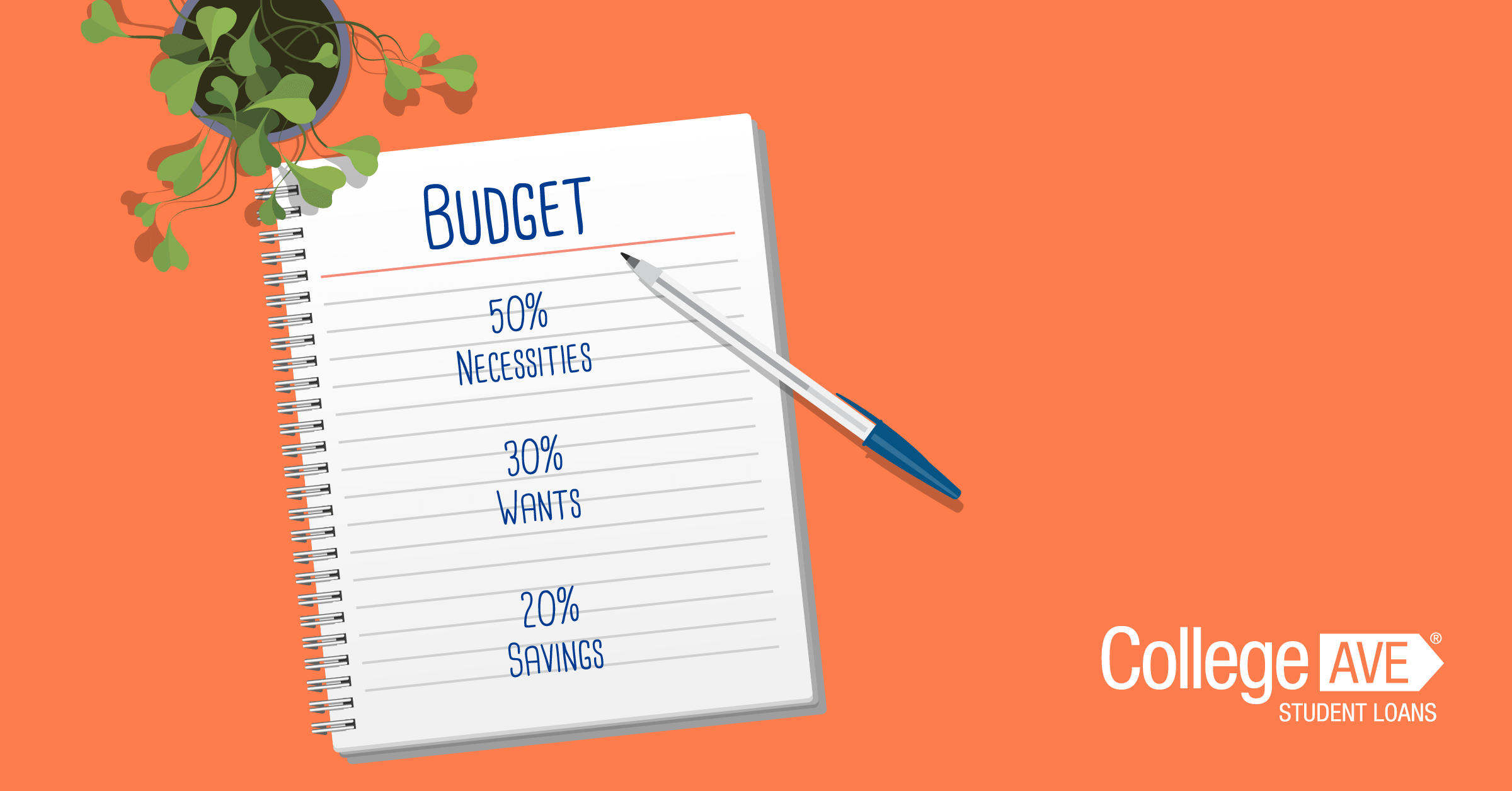

One budgeting strategy that has become increasingly popular is the 50/30/20 rule. Developed by senator Elizabeth Warren, the 50/30/20 rule is an easy-to-follow formula for organizing a budget and making sure you’re covering important expenses while still saving money each month.

How the 50/30/20 Rule Works

Warren, a former law professor that was part of the formation of the Consumer Financial Protection Bureau, first introduced the 50/30/20 rule in her book “All Your Worth: The Ultimate Lifetime Money Plan.”

Unlike other budgeting systems, which can be complex and extremely detailed, Warren designed the 50/30/20 structure to be simple and straightforward. It divides your income across three buckets: needs, wants and savings.

Budget 50% of Your Money for Absolute Necessities

Under Warren’s proposed budgeting plan, 50% of your net income — the amount of money you receive from your paycheck after taxes and other deductions are withheld — goes toward essential expenses. This category is for necessities, such as your rent or mortgage payment, groceries, utility bills, and transportation.

If you have any debt from credit cards, a car payment, or student loans, include the minimum required payments in this category.

Budget 30% of Your Money for “Wants”

It’s important to account for non-essential expenses so you get to enjoy yourself responsibly. With the 50/30/20 plan, you dedicate 30% of your net income to your wants, such as dinners out with friends, streaming service subscriptions, movie nights, or travel.

Budget 20% of Your Money for Savings

Finally, 20% of your net income should go toward your savings and financial goals. A common question people have is, “does the 50/30/20 rule include retirement?” The answer is yes; retirement savings are part of the 20% bucket.

Other forms of savings that fall into this category include:

- Building an emergency fund in a high-yield savings account

- Saving a down payment for a house

- Planning for future education expenses

Examples of the 50/30/20 Rule

Now that you know how the 50/30/20 works, let’s look at some examples of how it could be implemented at different income levels. In all three examples, the incomes listed are their net-after-tax incomes:

Sue, a Mental Health Counselor earning $48,000 per year

Sue’s gross income is $48,000 per year, or $4,000 per month. Based on that income, here is how she would divide her money under the 50/30/20 rule:

| 50% on Essentials | 30% on Wants | 20% on Savings | |

|---|---|---|---|

| Monthly | $2,000 | $1,200 | $800 |

| Annual | $24,000 | $14,400 | $9,600 |

John, a High School Teacher earning $60,000 per year

With an annual gross income of $60,000, John has a monthly income of $5,000 to work with to create his budget.

| 50% on Essentials | 30% on Wants | 20% on Savings | |

|---|---|---|---|

| Monthly | $2,500 | $1,500 | $1,000 |

| Annual | $30,000 | $18,000 | $12,000 |

Molly, a Dental Hygienist Earning $77,000 per year

Molly has the highest gross income of the three at $77,000 per year, giving her approximately $6,400 per month.

| 50% on Essentials | 30% on Wants | 20% on Savings | |

|---|---|---|---|

| Monthly | $3,200 | $1,920 | $1,280 |

| Annual | $38,400 | $23,040 | $15,360 |

Applying the 50/30/20 Plan to Your Own Life

To implement a 50/30/20 budget in your own life, you can use a free worksheet from the CFPB. You can also use simple tools through your bank, like an automatic monthly transfer from your checking to your savings account to ensure that you’re saving toward your 20% goal.

Is the 50/30/20 Rule Realistic?

Although the 50/30/20 approach to budgeting is popular because of how simple it is, it may not work for everyone. The designated percentages may not be realistic for people living in areas with high costs of living. For example, residents of New York City, Palo Alto in California, or Boston, Massachusetts may find that the 50% mark for essentials is too low. And if you have a significant amount of debt, such as high student loan payments, you may need to allocate more of your budget to debt repayment.

The 50/30/20 rule can also be difficult if you have a variable income. Hourly employees that may have seasonal spikes, freelancers, or those working in the gig economy may find it difficult to maintain a 50/30/20 budget since their income may not be consistent month-to-month.

If the 50/30/20 categories don’t meet your needs, you could adjust the percentages to better suit your lifestyle. For example, the 60/20/20 rule is a popular variation. It bumps up the allocation for essentials to 60% and cuts the budget for wants to 20%. At the end of the day, it’s more important that you find a budgeting system that works for you and your unique needs — one that you will stick with for the long haul.