If you recently graduated from college, congratulations! That’s a huge accomplishment. Now, there are no more tests to study for, no more early morning classes, and no more all-night study sessions.

However, you do have to start thinking about managing your student loans. Chances are you deferred payments on your student loans, which means that you weren’t required to make any payments while you were in school. If you deferred payment on your loans then your loans are typically granted a grace period, meaning you don’t have to start making payments just yet. But that grace period will come to a close, so it’s important to come up with a strategy to manage them.

7 things to do before your grace period ends

With most deferred student loans, you have a grace period after you graduate. This is a time when you don’t have to make payments on your student loans, giving you a few months to find a job. In many cases, a grace period is six months in length, but it can vary from lender to lender.

However, that grace period will be over before you know it, and you’ll have to start making payments on your loans.

To make sure you’re prepared, follow these seven tips before your grace period ends.

1. Find out who your student loan servicer is and how much you owe

When you were in college, you likely took out several different student loans to pay for school. Your student loan lender may not be your student loan servicer, so you’ll want to find out who your loan servicer is and how much you owe.

You can find out exactly how much student loan debt you have by using these two resources:

- National Student Loan Data System (NSLDS): The NSLDS is a central database of federal student loans. Just enter your information, and the NSLDS will list all the federal student loans in your name, including how much you owe and who your loan servicer is for each loan.

- Your credit report: Private student loans in your name will be listed on your credit report. You can review your report for free at AnnualCreditReport.com.

2. Contact your loan servicer

If you’ve changed your address or contact information since you were in school, your loan servicers may not be able to get a hold of you to tell you when your grace period ends, what your minimum payment is, and when your monthly payment is due. This could lead you to miss payments, subjecting you to late fees and damage to your credit.

To avoid any issues, reach out to the loan servicers you found on the NSLDS or your credit report to update or confirm your contact information.

3. Sign up for automatic payments

Once you contact your loan servicers, they can tell you how to create online accounts with them. Doing so will allow you to continuously monitor your accounts, keep track of your loan payoff progress, and even make payments online.

Signing up for automatic payments is a smart idea. Not only does it reduce the risk of missing a payment, but many lenders offer interest rate discounts if you sign up to make automatic payments. For example, College Ave will give you a 0.25% interest rate reduction when you sign up for autopay. Over the length of your loan repayment, the automatic payment interest deduction can help you save hundreds of dollars.

4. Create a budget

Once you know how many loans you have, who your loan servicers are, and how much money you owe each month, it’s important to come up with a comprehensive budget. Having a budget will ensure you live within your means and can comfortably afford your student loan payments along with your other essentials.

Your budget doesn’t have to use fancy software; just list how much income you have coming in each month after taxes on a piece of paper. Then, list all your recurring expenses, such as rent, groceries, utilities, car payments, student loan payments, health insurance premiums, clothing, and your cell phone bill.

If your expenses outpace your income, think of ways to cut back. You could get a roommate to reduce your housing expenses, downsize to a smaller cell phone data plan, or cook more at home. Or, boost your income by picking up a side hustle like delivering groceries or walking dogs.

5. Know your repayment options

Before your grace period ends, make sure you understand the repayment plan you chose when you applied for your student loan. Reach out to your lender and/or servicer to get a better understanding of your loan repayment terms and repayment options. If you have federal student loans and your monthly payment is too high, you may qualify for an income-driven repayment (IDR) plan.

With an IDR plan, the loan servicer extends your repayment term, and your monthly payment is capped at a percentage of your discretionary income. If you’re struggling to make payments, signing up for an IDR plan can dramatically reduce your monthly payment and give you more breathing room, but keep in mind it may increase the overall cost of the loan by extending the time it takes to repay it. Contact your federal student loan servicer for more information or you can apply for an IDR plan online.

6. Make payments right away, if possible

While the student loan grace period can give you time to find a job and get settled, you can save money by making payments during it, instead.

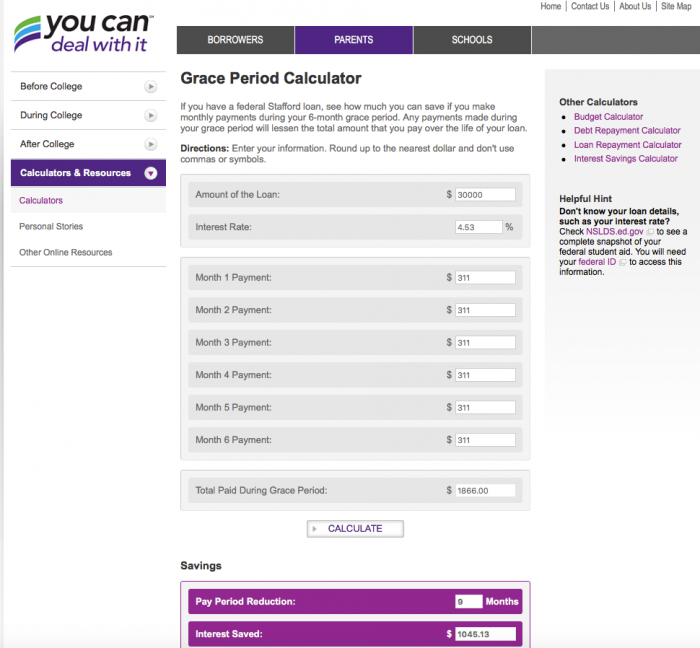

For example, let’s say you had $30,000 in federal Direct Unsubsidized Loans at 4.53% — the current interest rate as of July 1, 2019. Under a standard 10-year repayment plan, you’d have a monthly payment of $311.

If you started making payments right away rather than waiting out the grace period, you could pay off your loans nine months ahead of schedule. Even better, you’d save $1,045.13 in interest charges.

If you can’t afford to make full payments during the grace period, try and pay whatever you can. Paying even just $25 a month can help cut down on how much you pay in interest charges.

7. Consider student loan refinancing

Some of your student loans may have high interest rates. A high interest rate can mean higher monthly payments, and you can end up repaying far more than you originally borrowed when you were in school.

If you have loans with high interest rates, consider student loan refinancing. With this strategy, you take out a loan for the amount of your current debt. If you have good credit, you can qualify for a loan with a lower interest rate, helping you save potentially thousands of dollars and pay off your loans ahead of schedule. To find out how much you can save, check out our student loan refinancing calculator.

There are some drawbacks to refinancing, especially if you have federal student loans. But if your loans have high interest rates, the benefits may be well worth it. Make sure you consider whether you’ll use any of the benefits that come with federal student loans like public service forgiveness or income driven repayment plans. Those benefits are no longer available once you refinance federal loans with a private lender.

Managing your loans

Your student loan grace period will be coming to an end soon. To ensure you’re ready for it and can handle your monthly payments, follow the above steps and come up with a repayment plan that works for you.

If you find yourself having trouble making payments on your student loans, don’t ignore the problem. Reach out to your student loan servicer to address the problem and try to work out a payment plan.

Looking to get rid of your debt as quickly as possible? Learn about how to repay your student loans fast.