Student loans can build credit and are one of the first ways many people get started building credit. Making regular on-time payments can lay the foundations of a good credit score for many years to come.

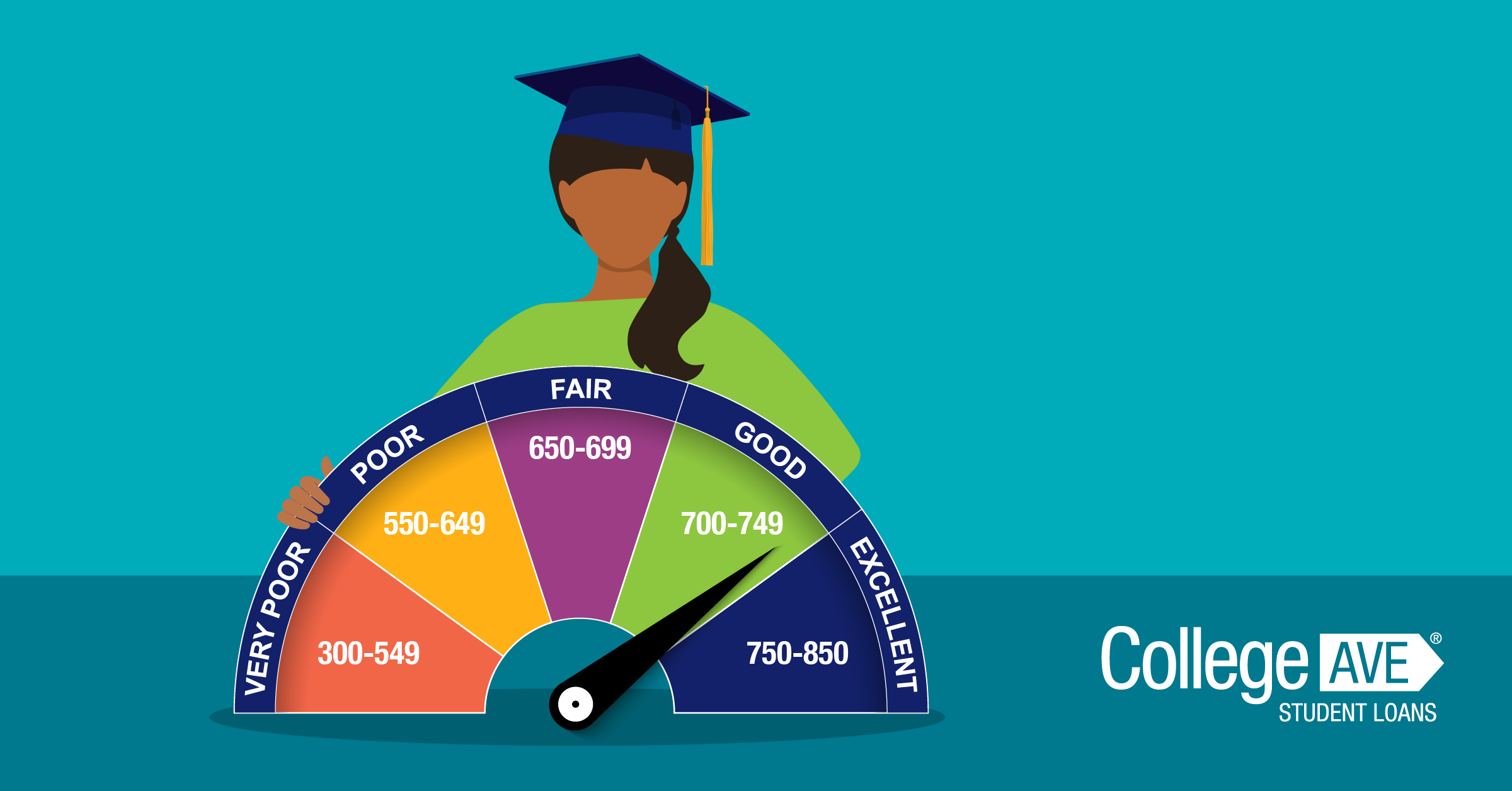

Credit is a measurement of a person’s financial risk. It indicates their likelihood to repay loans in full and on time. Credit is one of the criteria private lenders look at when deciding whether to lend to someone. But having good credit doesn’t just make you eligible for some student loans, it opens doors to other financial products and possibly a less expensive future.

With good credit you can get lower rates on loans for homes and cars, credit cards, and insurance premiums. And if you’re looking for an apartment, a good score can make renting a lot easier.

Building credit is just as important to a student’s future as getting good grades, but it can be just as challenging. So, let’s take a closer look at how student loans can be used to help build a positive credit score.

Building Credit as a New Student

Establishing credit is hard, especially without having much of a financial history. But don’t feel alone, many students are in the same boat. This can feel frustrating, especially when some students need credit to access some of the financial products they can use to help cover the costs of college. But new students can’t get credit until they have a financial history. So, how can you get started?

- Get a Secured Credit Card: A secured credit card is a type of credit card that is backed by a refundable security deposit. The cash deposit reduces the card issuer’s risk. Generally, your security deposit will double as the card’s spending limit and ensures that you have the funds to pay back what you charged. This is a great way to establish and start building credit with the funds you already have.

- Consider a Student Credit Card: Student credit cards are simply credit cards that are made for students. They typically have lower credit limit to allow students to practice responsible use and repayment.

- Make Payments on Time: No matter which option you choose, it is essential that you make timely payments. This is a big signal to lenders that you can pay back that debt and pay it on time. It takes time to develop the credit portfolio needed to take out private student loans on your own. Even when undergraduates do qualify, often they’ll qualify for lower interest rates by using a co-signer with a stronger credit score. When a co-signer is involved, both parties can use the loan to build their credit.

TIP: Here are a few more ways new students can start building credit.

How Does Paying Student Loans Build Credit?

There are three ways student loans can help build credit.

- Lowering Perceived Risk.

Making payments on time shows credit bureaus good financial management. This reduces the perception of risk in doing business with you. When a report has few other items, which is the case for many students, on time loan payments contribute to credit score growth by showing your commitment to repay debt. - Increasing Average Account Age.

Most credit bureaus consider the “average account age” to build credit reports. This rewards the length of a person’s credit history, people with a longer credit history are seen as less risky than those with shorter or no history at all. Because student loans are paid off over a number of years, they help increase the average account age and with it the credit score. - Adding Credit Mix.

Another standard that credit bureaus evaluate is the diversity of credit types in your portfolio. For example, student loans are considered an “installment” account because they are paid off over time. Credit cards are a “revolving” account type where there is a minimum due and the balance gets rolled over. Having a mix of account types contributes to building good credit.

TIP: Here’s an article that goes into more detail about how credit scores are determined.

Can Student Loans Hurt Your Credit?

Making on time payments can help your credit, but late or missed payments can hurt and lower your credit score. Loans that go into default can cause long-term harm, making things like home loans, credit cards, and car loans more expensive to borrow down the line.

It’s important to be realistic about your ability to make payments. When it’s hard to keep up, ask your lender about deferral, forbearance, and other types of payment relief before going into default and damaging your credit.

It’s important to know that applying for credit products like private student loans can temporarily lower credit scores. Each time a loan is applied for, a “hard pull” is conducted on the applicant’s credit report. A hard inquiry is just a record that a company or lender accessed and evaluated your credit. It’s not the most important factor that goes into scoring credit, but they can be considered negative. Even applicants with solid, established credit may see their credit score temporarily lower after a hard credit pull.

TIP: If you’re shopping around for the best private student loan rates applications typically within a short period of time, such as within a 30-day window, are usually considered as one credit inquiry instead of multiple inquiries. This allows you to check and compare lenders to find the best loan terms.

Some lenders offer borrowers a way to prequalify without going through a hard pull. This can be a really helpful tool when comparing options because it only conducts a “soft pull” which does not impact the credit score. With pre-qualification, applicants can see an estimated interest rate or range based on their credit, but without receiving the negative impact of undergoing a hard pull.

TIP: Try our prequalification tool to see what your rates could be.

Lasting Impressions

Making that last student loan payment is an incredible financial achievement that leaves a lasting impression on your credit report. While it’s common to see a brief dip in your credit score right after, what’s more important is the long-term value of the paid-off loan, which stays on your credit portfolio typically for ten years. All the hard work put in to making punctual and regular payments keeps a powerful record of good financial management on your report, helping build your score overall.

Check out these tips for building credit that every student should know.