What Are Some of the Best Ways to Increase My Credit Score?

Credit scores aren’t written in stone; they’re a snapshot of your credit file at the time the score is requested. Your credit score can go up or down (or stay the same) as your credit file is updated with new information. So, if you currently have a low score, it doesn’t mean it has to stay low forever. On the flip side, if you have a high score, it doesn’t mean you can stop being responsible with your credit!

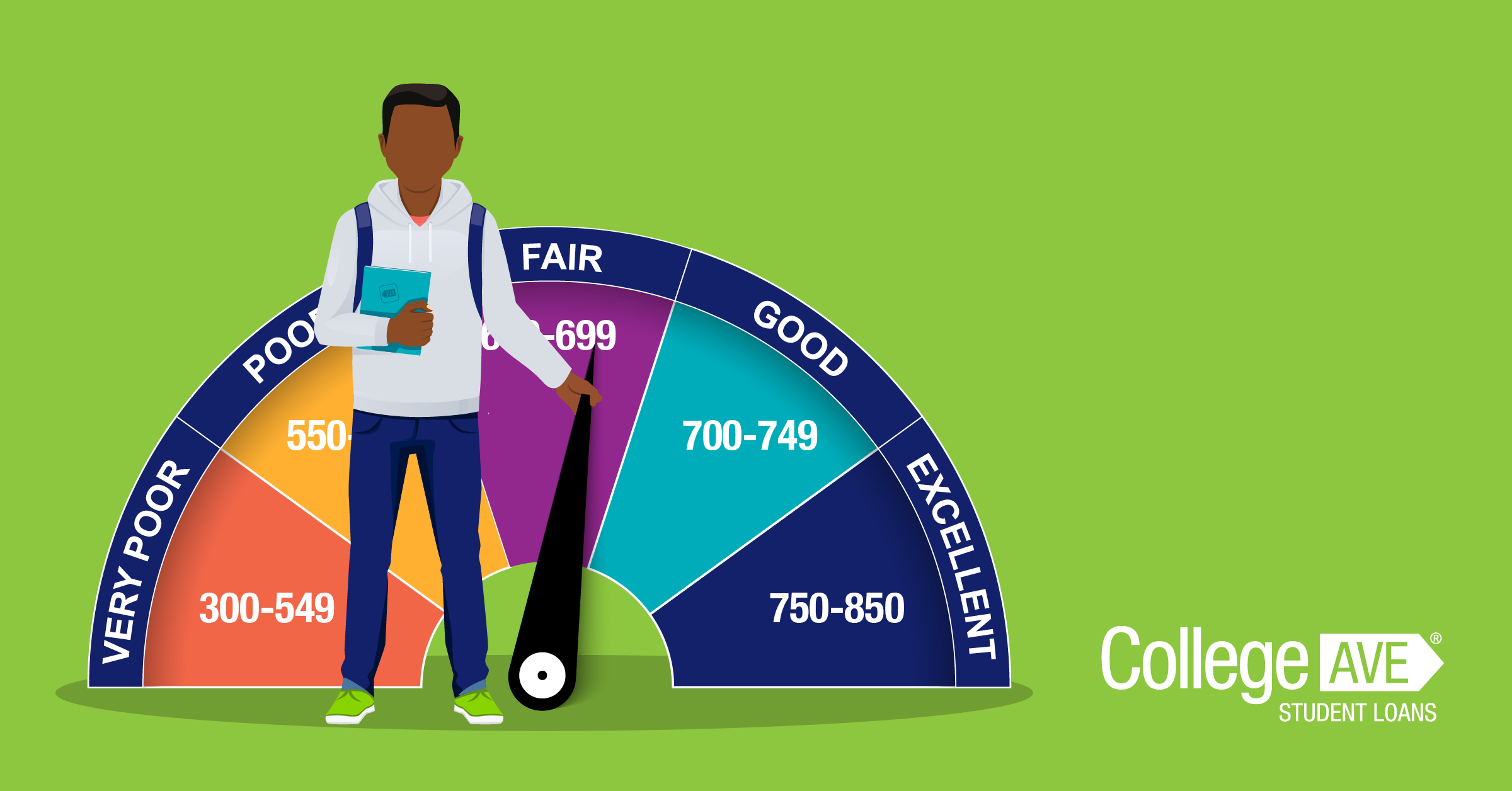

Some students have a poor – or even non-existent – credit score because they simply do not have an established credit history, and this is completely normal – especially for high school and college students. Other times, an individual may have misused credit in the past (such as racking up a big credit card bill and never paying) and their credit score suffered as a result.

In either case, college students need to know how to improve their credit score. Below are some of the best ways you can increase your credit score, along with tips to help maintain a good credit score once you have one.

Recommended Reading: What is a Credit Score?

Establish Credit Early

Starting to build your credit history early – while in high school and college – will help in the long run as length of credit history typically accounts for 15% of your total score.

Your parents or trusted family members may be able to help you establish credit.

- Cosign A Loan: Parents can cosign a loan with their child and ensure they make their payments on time.

- Authorized User on A Credit Card: Your parents can add you as an authorized user to a credit card where someone is consistently making payments. Payment history will be added to your credit file. This shows that you can make payments regularly and you can pay them on time. It’s important to know that only some credit scores consider these payments for your credit history.

- Put Bills in Your Name: If you live off-campus in a house or apartment, you may be able to put your cell phone, utility or rent bills in your name. When you make regular monthly payments, this helps to build a positive history on your credit report. It’s important to know that only some credit scores consider these payments for your credit history.

Make Consistent Student Loan Payments

Making payments toward your student loans is one of the first ways you can start to build serious credit. According to the National Council for Credit Counseling, having a history of on-time student loan payments helps build your payment history, which typically accounts for 35% of your score. Making inconsistent or late payments, as well as defaulting, can bring your score down.

Tip: Setting up automatic payments makes paying on time a lot easier, plus many lenders, such as College Ave, offer a 0.25% interest rate reduction for setting up auto-pay.

Shop for a Loan Within a 45-day Window

Whenever you apply for a student loan, there is a hard inquiry on your credit file, also referred to as a hard credit pull. Hard credit pulls can temporarily lower your credit. However, FICO, which is the most common credit score used by credit bureaus, uses a 45-day de-duplication window, beginning at the time of the first inquiry. So, if you want to shop for a student loan from different lenders, doing so within a 45-day window will result in only one inquiry impacting your credit score.

Make More Than Student Loans a Part of Your Credit History

You may notice a dip in your credit once you’ve made your last student loan payment. This is common and occurs when your student loan payments were used as the main driver of your credit score. With little credit history outside of the loan, your credit history shrinks, a factor that typically accounts for 15% of your score.

It’s a good idea to build a positive payment history outside of any student loans. A mixture of credit types – such as credit cards, car loans, and student loans – that are well maintained with good payment history helps to show lenders that you’re financially responsible.

Tip: Don’t take on more debt than you need just to increase your credit score.

Keep the Right Balance on Your Credit Cards

Credit utilization is the amount of credit being used compared to the maximum amount allowed. Keeping your credit utilization in the right zone typically accounts for 30% of your credit score. Maxing out a card, or holding a very high balance, can negatively impact your credit.

Tip: Make it a rule to never have more than 25% of your credit limit in use on any one card. To help manage this, some credit card providers allow you to set alerts when a certain amount of credit is being used.

Request an Increase in Your Credit Limit

If you are responsible with your credit card and maintain a low balance but still want to improve your credit score, you can ask for an increase in your credit limit. When you increase your credit limit but continue to spend the same (or less) as you did before, you will improve your utilization ratio.

If You’ve Had Problems in the Past, Re-establish Your Credit History

Negative items typically fall off your credit report after seven years, some items such as certain bankruptcies can take ten years, leaving you with a clean slate to re-establish a healthy credit history.

Through the Fair Credit Reporting Act (FCRA), the Federal Trade Commission requires the three national credit reporting bureaus – Equifax, Experian, and TransUnion – to provide consumers with a free copy of your credit report every year. It’s a good idea to look for potential errors on your credit report annually so you can file a report to fix any incorrect information. You can even get your credit reports online for free.

Pay Down Existing Debt

Your credit score takes into account the amount of the debt you may owe compared to the original amount you borrowed for any loans. Paying down your debt will help to improve your score. Use unbudgeted money, such as a bonus or tax refund, to make additional payments on your debt.

Don’t Close an Old Credit Card that Has a Zero Balance

Keeping an old credit card open that you don’t use could help your credit score more than closing it. By leaving the card on your file, you are helping to improve your utilization ratio and age of your credit file.

Recognize your situation when deciding to keep a card open. If you’re trying to clean up your credit and think you might be tempted to irresponsibly use the card, keeping it open might not be the best decision for you.

Always Pay Your Bills on Time!

It may seem obvious but making timely payments on any debt is the golden rule of how to improve your credit score.

Set up automatic bill pay when possible to ensure you don’t forget to pay your bills – plus it saves you time. You can also set a recurring reminder on your phone or your calendar in advance of the due date to ensure you make your payments on time.

It’s a good idea to monitor your credit because building your score takes time. Armed with these tips, you’ll have a better chance to continually improve your credit score.