If you’re in the process of looking for a student loan (or any loan for that matter), there’s a good chance you encountered your credit score – a three-digit number commonly used by lenders to predict the likelihood that you will pay the amount due on time.

Your credit score is often a driving factor in determining whether a lender will extend you credit, and if so, at what interest rate. Usually, the better your credit score, the lower the interest rate you’ll be offered. But what components actually make up your credit score, and how can you improve it?

What components make up my credit score?

The most commonly used credit score is the FICO score – created by the Fair Isaac Corporation.

The main factors that influence your FICO credit score can be broken down into five different categories:

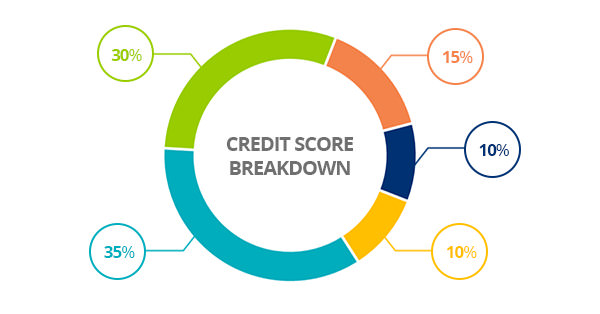

Payment History

This is a reflection of whether your prior bills were paid on time, how many were sent out for collection, and any bankruptcies. It also takes into consideration any other debt obligations you may have, such as a credit card, car loan, or mortgage, and whether or not those bills were paid on time. When these events happened also affects the score. The more recent the event, the more impact it has on your credit score.

Total Credit Score Impact: 35%

Debt Amount Owed (Utilization)

This refers to the amount of credit utilized compared to the amount of credit available. For example, owing $5,000 on a $10,000 credit line results in a 50% utilization. Essentially, if a high percentage of your credit limit is being utilized, it can indicate that you may be overextended and have a higher chance of missing or making late payments. This is also one of the easiest factors to improve and fastest means of increasing your overall credit score.

Total Credit Score Impact: 30%

Length of Credit History

The longer the credit history, the better it is for the overall credit score. Credit history length refers to the age of a specific credit card or other line of credit. It will include both the age of your oldest and newest credit account, among other things. While having a short credit history doesn’t automatically result in a low credit score, if you’re striving for a perfect score, having a long and well-established credit history is absolutely necessary (SubscriberWise).

Total Credit Score Impact: 15%

New Credit/Inquiries

Every time you apply for a new credit card, mortgage, student loan, or other form of credit, a credit inquiry is created. An inquiry is when a lender obtains your credit report from one of the bureaus after you request credit from them. Hard credit inquiries can impact your score, so you want to be smart when shopping for credit. Newly opened credit accounts will also have an impact.

Total Credit Score Impact: 10%

Types of Credit

This refers to the mix of credit types on your account. Car loans, mortgages, credit cards and student loans are all seen as different types of credit in the eyes of the credit reporting bureaus. Having a good mix of financial responsibilities and handling them responsibly could improve your credit score.

Total Credit Score Impact: 10%

Different Types of Credit Inquiries and How They Are Generated

There are two different types of credit inquiries: hard inquiries and soft inquiries. It’s important to know the difference between the two and how each affects your credit score.

Hard inquiries are the ones that can affect credit scores and are generated by shopping for credit. They indicate if an individual is actively trying to get a credit card, student loan, etc.

Soft inquiries do not affect credit scores and aren’t generated by shopping for credit. Examples of soft credit inquiries include employer-generated or insurance company-generated inquiries, pre-approved inquiries, account reviews by lenders with whom you already have an account, and whenever an individual checks their own credit score.

College Ave Student Loans offers a credit pre-qualification tool where you can see if your credit qualifies prior to applying. This is an example of a soft inquiry that does not affect your credit score.

What if I want to apply for multiple student loans? Will that hurt my credit score?

If you want to apply for multiple student loans to shop your interest rate, there is a way to do this without affecting your credit score with multiple inquiries.

FICO uses a deduplication window of 45 days, beginning at the time of the first inquiry. What this means for students is that all student loan applications resulting in pulled credit reports (hard credit inquiries) within a 45-day period will only count as one inquiry on a credit report rather than multiple.