Changes are coming to the 2024-2025 Free Application for Federal Student Aid (FAFSA). So, to help families better understand what to expect, I’ve pulled together an easy guide to help prepare for the changes.

The 2024-2025 Free Application for Federal Student Aid (FAFSA) will be much simpler than previous versions of the FAFSA and involves changes to both the financial aid form and formula.

So you can plan ahead of time, it is important to understand how changes to the FAFSA may affect your eligibility for need-based financial aid. Some of these changes will increase financial aid eligibility for low-income students, while other changes will decrease aid eligibility for some middle- and high-income students.

Part of the rationale behind the changes to the FAFSA is the complexity of the current form and how the experience serves as a barrier to college access by low- and moderate-income students. The old FAFSA was longer and more complicated than federal income tax returns. The new FAFSA will be much shorter.

TIP: Just getting started on the FAFSA? Read all about how to apply with College Ave’s comprehensive guide.

What is the FAFSA Simplification Act?

Senator Lamar Alexander, who was chair of the Senate Health, Education, Labor, and Pensions (HELP) committee, has long been a proponent for simplifying the FAFSA. To celebrate his retirement, Congress included his proposals for simplifying the FAFSA as part of the Consolidated Appropriations Act, 2021.

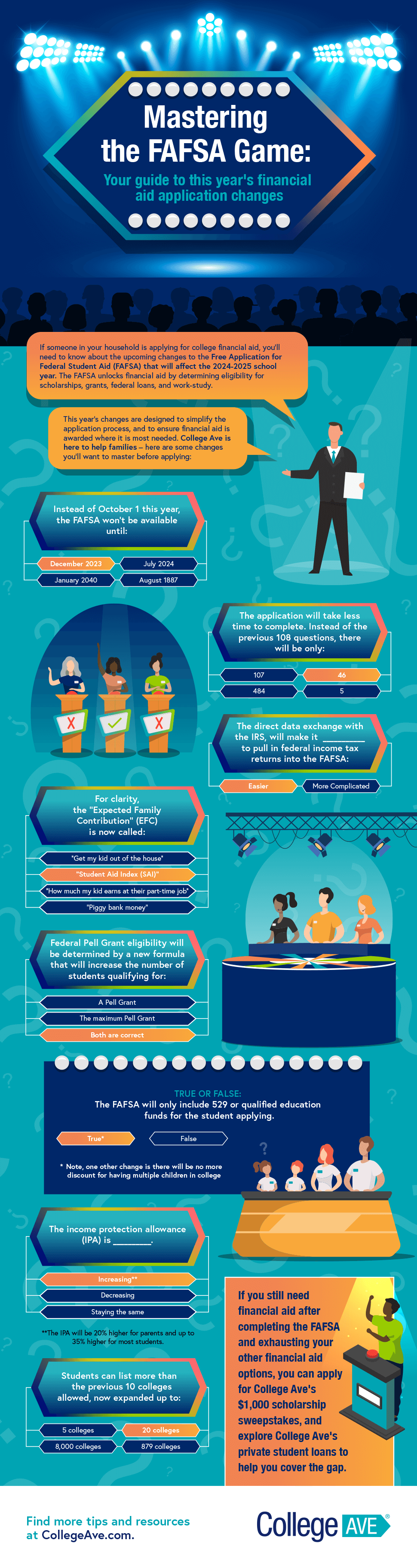

These changes will go into effect for the 2024-2025 FAFSA. However, due to the complexity of simplifying the FAFSA, the start date for the 2024-2025 FAFSA will be delayed from October 1, 2023, to December 2023. The FAFSA will return to an October 1 start date in the years following.

Major Changes to the FAFSA in 2023

1. The FAFSA will be much shorter, less than 50 questions instead of 108.

Students and parents should find the new FAFSA to be much easier to complete. The draft of the new FAFSA has 46 questions. However, many applicants will not need to answer them all, due to intelligent skip logic and other smart solutions implemented as part of FAFSA simplification.

The new FAFSA will be better aligned with federal income tax returns, allowing the answers to these questions to be transferred from the IRS to the FAFSA. The IRS data retrieval tool will be integrated into the new FAFSA and mandatory. The capabilities of the IRS data retrieval tool will be expanded to enable it to handle changes in marital status that occur after the tax year upon which the FAFSA is based.

The new FAFSA also eliminates many questions that affected less than 1% of applicants.

All of this will yield a simpler FAFSA, eliminating about two-thirds of the questions.

2. Expected Family Contribution (EFC) is now referred to as the Student Aid Index (SAI).

The new FAFSA will show a Student Aid Index (SAI) figure instead of the Expected Family Contribution (EFC).

This name change will eliminate a source of confusion, where families incorrectly thought that the EFC was all that they would need to pay. Many families pay more than the EFC, since most colleges leave students with a gap of unmet need and even colleges that meet full need include loans as part of the financial aid package.

There are some changes in how the SAI will be calculated. In addition to eliminating many data elements on the FAFSA, the financial aid formula will shelter more of the family’s income from need analysis. On the other hand, the number of children in college at the same time will no longer affect the SAI. There is also a change in how eligibility for the Federal Pell Grant is determined.

3. Pell Grant eligibility will be determined by a new formula.

The new FAFSA is adding a second formula for calculating eligibility for the Federal Pell Grant in addition to the old formula.

The new formula, which compares income to a multiple of the poverty line, will increase the number of students qualifying for a Federal Pell Grant. It will also increase the number of students qualifying for the maximum Federal Pell Grant.

4. No more discount for having multiple children in college at the same time.

Senator Alexander was adamant that families should not qualify for more financial aid simply because of the timing of their children.

Under the old formula, the parent contribution portion of the EFC was divided by the number of children enrolled in college at the same time. This meant that going from one child in college to two children in college was almost like dividing the parents’ income in half. But a family with children separated in ages by four or more years did not receive the same financial benefit.

This loophole mainly benefited middle- and high-income families. Low-income families did not benefit because they had a very low or zero EFC. Moreover, the increase in aid eligibility was greater for high-income families than it was for middle-income families.

About half of families who have multiple children in college had at least one year of overlap among them. This loophole could increase eligibility for need-based financial aid by thousands of dollars for high-income families.

Families can still appeal for more financial aid based on having multiple children in college simultaneously, but most colleges will not make an adjustment except in unusual circumstances. For example, they might make an adjustment if the parents are enrolled in college at the same time as their children, in which case they might subtract the costs paid by the parents for their own education from income. (College financial aid administrators cannot make changes to the financial aid formula, so they will not be able to divide the parent contribution by the number in college.)

5. The parent who fills out the FAFSA will change dependent on divorce or separation.

Currently, the parent responsible for completing the FAFSA is the parent with whom the student lived the most during the 12 months ending on the date the FAFSA is filed. If the student lives equally with both parents, then it is based on whichever parent provides more financial support. If that doesn’t distinguish the parents, then it is the parent with the greater income.

Due to better alignment of the FAFSA with federal income tax returns, the parent responsible for completing the FAFSA will be the parent who provides more financial support to the student. After all, the FAFSA is a financial form, so it makes sense to follow the money.

6. The financial aid appeals process is changing.

College financial aid administrators can no longer have a policy or practice that denies all financial aid appeals. Instead, they must consider each financial aid appeal on a case-by-case basis.

For example, some community colleges would deny appeals from students who were quitting their jobs to enroll in college full-time. By ignoring these appeals, the colleges blocked the students from qualifying for a Federal Pell Grant, which would have made the college much more affordable and increased college graduation rates. Students who work a full-time job in college are half as likely to graduate, as compared with students who work 12 hours or less a week.

College financial aid administrators cannot limit adjustments to just the data elements on the FAFSA. They must allow adjustments to the cost of attendance when appropriate. For example, if a student appeals for an increase in the allowance for textbooks, transportation, dependent care or special needs, the financial aid administrator must consider an adjustment to the cost of attendance.

Dependency overrides are assumed to continue from one year to the next, unless there is conflicting information, or the student says that their circumstances have changed. In addition, colleges can rely on a dependency override made by a financial aid administrator at another college in the same or previous award year. Colleges must evaluate a request for a dependency override within 60 days of the start of the student’s enrollment.

Determinations of homelessness must be made without regard to the reasons why the student is an unaccompanied and/or homeless youth.

7. Income protection allowance is increasing.

The income protection allowance (IPA) shelters a portion of student and parent income from the financial aid formula. The IPA is increasing for both students and parents.

The IPA will be 20% higher for parents and up to 35% higher (up to about $2,400 higher) for most students. However, the IPA will be up to 60% higher (up to about $6,500 higher) for students who are single parents.

8. The myStudentAid App will retire.

This is more of a technical change to the FAFSA, but it should make the process easier.

The U.S. Department of Education has retired the myStudentAid App because it was not used by enough students to justify its continued existence. Instead, the responsive design of the StudentAid.gov website allows students to complete the FAFSA more easily than before on mobile devices. The StudentAid.gov website automatically resizes to fit the screen size and shape of mobile phones, tablets, laptops, and desktop computers.

The Bottom Line…

These changes to the FAFSA will bring many updates to the financial aid application, which will make it easier and quicker to apply for federal student aid. It will also reduce the likelihood that a student’s FAFSA is selected for verification, saving families time and hassle. More students will qualify for a Federal Pell Grant, and more of them will qualify for the maximum grant. If you still are in need of financial aid after completing the FAFSA, you can apply for College Ave’s $1,000 scholarship sweepstakes or look into College Ave’s student loans to help you cover the gap.