If you’re shopping around for private student loans, you’ve probably encountered questions about your “credit score.” Your credit score is a three-digit number that summarizes information about your credit history, which is available in your credit report.

To better understand how your credit history and credit report are used to calculate your credit score, let’s first address the question: What does a credit score mean?

What is a credit score?

A credit score is a calculation that indicates the likelihood that you will repay a loan in full and on time. In other words, your credit score is a “grade” for your “creditworthiness.”

This can affect not just the amount a creditor is willing to lend you, but your interest rate on that amount, which affects the total cost of your loan. For example, lower credit scores tend to receive higher interest rates, which means you’ll pay more in interest charges over the life of your loan.

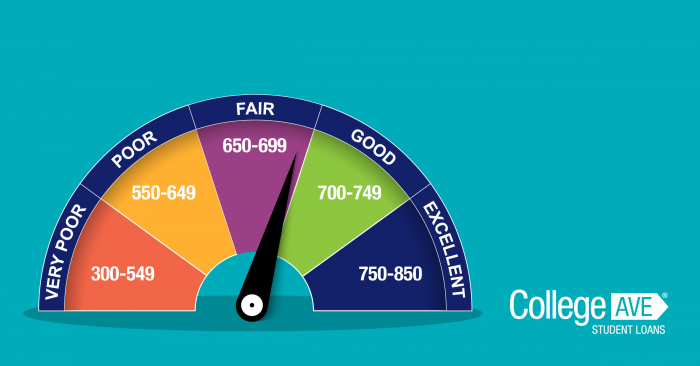

What’s a good credit score?

Many companies can generate credit scores. Some of the most commonly known scores are FICO scores. FICO stands for Fair Isaac Corporation, the creators of the score, which has a range of 300 to 850 (with 850 representing the best and highest credit score).

There are three national credit-reporting bureaus that issue a FICO score:

Lenders usually work with one of the three bureaus to obtain your credit score. A lower credit score suggests a greater risk that you will not fully repay your loan (or repay it on time), whereas a higher credit score suggests a stable financial situation and less risk.

Every lender will have their own set of criteria for assessing the level of risk they’re willing to tolerate when extending credit. For example, one lender might elect to issue loans only to individuals with a score higher than 700, whereas another lender might consider individuals with a score higher than 640.

What’s the average credit score for a typical college student or high school graduate?

According to Credit Karma, the average credit score for people between the ages of 18 and 24 is 630. The average credit score for people between the ages of 25 and 34 is slightly lower at 628. As of the latest Credit Karma reporting, the first age group to break a credit score of 630 is between the ages of 45 and 54, with an average credit score of 646.

How are credit scores calculated?

Your credit score is calculated using information in your credit report. This report includes your entire credit history – mortgages, car loans, student loans, credit cards – any type of credit that has ever been extended to you, and any payments related to that credit (missed, late, or on-time).

Overall, a good credit history paints a picture of stability. The longer you’ve been using credit responsibly, the better that is for your score. Likewise, an extended history of missed or late payments can hurt your credit score.

There are a number of components in your credit history that contribute to the calculation of your credit score. Not all of these components weigh equally, so it’s important to understand how each factor in.

Payment History – 35% of your credit score (highest of all components)*

One of the most important components of your credit report is your payment history. This shows which payments to current and former creditors you have paid on time and which (if any) you have not. These details can date back years.

Debt Utilization Ratio – 30% of your credit score*

Your debt utilization ratio shows how much credit has been extended to you at the time a credit report is run, and how much of that credit you are using. The more credit you have that you are not using, the better. Some experts advise sticking to no more than 10% credit utilization while others say 30% is good.

NOTE: Credit utilization applies to revolving credit, as opposed to installment loans. Student loans are considered installment loans, so if you have two credit cards plus one student loan and you are not carrying a considerable balance on either card, that bodes well for your credit score, as follows:

| Credit Type | Amount Issued | Amount Used (Balance) | Percentage Used |

| Credit Card 1 | $5,000 | $500 | 10% |

| Credit Card 2 | $10,000 | $2000 | 20% |

| Student Loan | $7,500 | $7,500 | n/a |

| Overall Credit Utilization | 15% |

Length of Your Credit History – 15% of your credit score*

A longer credit history can contribute to a higher credit score – particularly if that credit history demonstrates using credit responsibly. While having a short credit history does not automatically result in a low credit score, if you’re striving for a perfect score, having a well-established credit history will be necessary (SubscriberWise).

New Credit/Inquiries – 10% of your credit score*

An inquiry is when a lender obtains your credit report from a credit bureau after you request credit from them. Every time you apply for a new credit card, mortgage, student loan, or another form of credit, a credit inquiry is generated.

There are two types of credit inquiries, and they affect your credit score differently:

- Hard inquiries are the ones that can affect scores. They indicate if an individual is actively trying to get a credit card, student loan, etc.

- Soft inquiries do not affect your credit score. Examples of soft credit inquiries include employer-generated or insurance company-generated inquiries, pre-approved inquiries, account reviews by lenders with whom you already have credit, and whenever you check your own score.

College Ave Student Loans offers a pre-qualification tool where you can see if your credit is likely to qualify prior to applying. This is an example of a soft inquiry that does not affect your credit score.

Types of Credit – 10% of your credit score*

Car loans, mortgages, credit cards, and student loans are all seen as different types of credit in the eyes of the credit reporting bureaus. Having a good mix of financial responsibilities and handling them in a trustworthy manner could improve your credit score.

* See Fico.com and FicoScore.com/FAQ for more information about this breakdown and other aspects of your credit score calculation and usage.

How do I build up my credit history and score?

It takes time to build your credit history. If you recently checked your credit score and found that it is low (or even nonexistent), you’re not alone. High school and college students typically have a limited credit history because they simply haven’t needed or had the ability to formally borrow from an established lender before. If you’ve never had a car loan, mortgage, credit card, or another form of credit, you won’t yet have a credit history and – as a result – a credit score.

There are a few ways that you can establish a credit history and build up your score. One way is to have a parent or legal guardian with good credit cosign a loan or credit account with you. Even if you don’t use the account, you’ll start building credit history as payments are made on time. This is called “piggybacking,” and it should ideally be done using a family member or spouse’s credit account.

How can I get a private student loan with little or no credit history?

If you have a low credit score – or no credit score at all – it is unlikely that you will qualify for a private student loan on your own, but that doesn’t mean you can’t get one. It means you’ll probably need to find a cosigner.

A cosigner is an individual – often a parent or legal guardian – who will sign the loan with you and take equal responsibility for it. Since your cosigner’s credit score can affect your interest rate, it’s wise to approach someone with a solid credit history.

Information about your loan will appear on both your and your cosigner’s credit reports, so keep in mind that any missed payments on your end could directly affect your cosigner’s good credit. Learn more about private student loan cosigners.

Can my credit score change?

Your credit score can change many times over. In fact, your credit score represents only the latest “snapshot” of information contained in your credit file at the time it was requested. Since your credit file is updated continually with new information, your credit score will fluctuate.

Your score is also typically different depending on which credit-reporting bureau is providing the information. Each might not have the same exact credit information on file for you. As a result, credit scores pulled from each of the three bureaus on the same day at the same time can differ.

Maintaining Your Credit Score

It is very important to understand, manage, and protect your credit score. Currently, you can request one free credit report per year from each of the main reporting bureaus. This type of self-inquiry will not affect your credit score. Reviewing your credit report annually is free and it’s a good way to get ahead of errors and inconsistencies.

Just as it can take years to elevate your credit score, it can take many years to rebuild a damaged score, so the key is to make smart credit decisions early on. And don’t be intimidated by a low credit score! Start building your credit history early, make smart credit decisions, and watch your score grow.