Throughout your college and student loan application process, you’ll likely encounter some unfamiliar terms and acronyms. EFC might be one of those acronyms and it’s found right in the Free Application for Student Aid (FAFSA).

What does EFC stand for?

EFC stands for Expected Family Contribution. This is the amount your family is expected to contribute toward your college education. The Department of Education uses this number to determine your “Financial Need,” which influences the types of federal, state, and institutional aid you can access and, in some cases, the amount.

How do I calculate my EFC?

You don’t have to calculate your expected family contribution on your own. Your EFC amount is determined through information you submit on your FAFSA, so you’ll need to fill out that form completely and accurately to ensure your EFC is calculated properly.

Several factors about your household are considered to calculate your expected family contribution, resulting in an “index” number that represents your family’s overall financial “strength.”

These factors include:

- taxable income

- untaxable income (e.g.: social security benefits, retirement income, etc.)

- cash, savings, investments

- real estate and business net worth (in certain instances)

- number of people in your household

- number of people in your household enrolled in college or expecting to attend college in the coming year

Generally speaking, the lower your EFC, the higher the amount of aid you can expect to receive. That is not a hard-and-fast rule, however. Your EFC will always be viewed in the context of the costs of a given school, and that can vary.

Will my EFC be different from school to school?

Your EFC is calculated from your FAFSA and remains consistent for all schools since the same data is sent to each of the institutions you choose on your application.

What will vary from school to school is your COA – or, Cost of Attendance. Your cost of attendance is an estimate of the total cost provided by a school to attend for a specific period. The school will typically consider your EFC when compiling your award package, but they’re not required to provide a specific amount of corresponding aid.

As a result, your actual family contribution can vary based on available funding at each individual school and the COA at that institution.

Your EFC, Your COA, and Your Financial Need

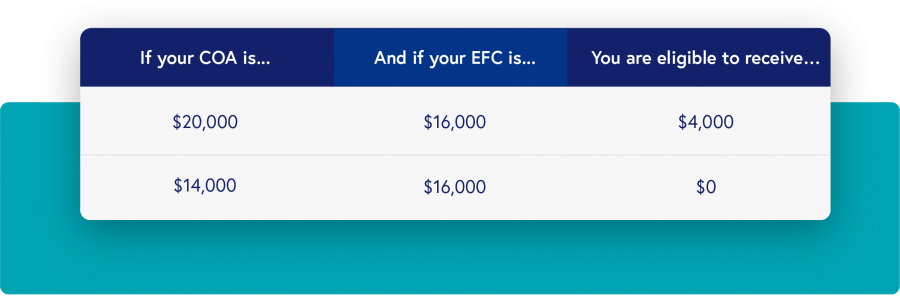

Since your EFC is subtracted from your COA at a given school to determine your financial need, your school selection can make a big difference in how your EFC affects the aid you are eligible to receive.

If a school’s cost of attendance comes close to your expected family contribution, you might not be eligible to receive any need-based financial aid. Conversely, a private university with significantly higher costs can elevate your financial need. You cannot receive more need-based federal aid than the amount of your financial need.

For example:

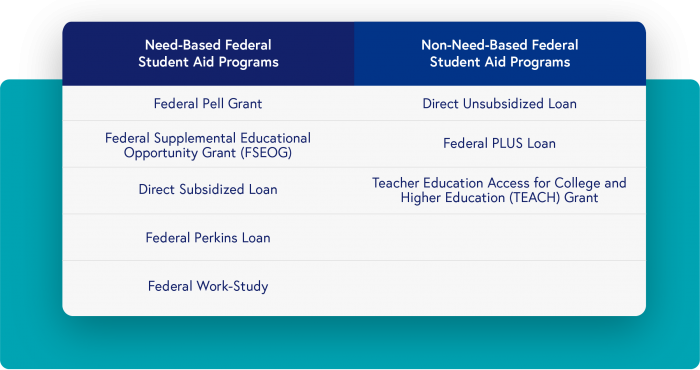

What if my EFC is too high to receive aid?

Remember that a high expected family contribution can result in low financial need. If your financial need turns out to be too low to receive need-based aid, you might qualify for federal assistance programs that are non-need-based.

Keep in mind that with or without federal student aid, many families find it challenging to cover the costs of a college education. These costs can include tuition, housing, textbooks, meals, loan fees, transportation, and more.

When your student aid package falls short of covering these costs, federal grants – like Pell Grants, which do not have to be repaid – can help make up the difference, as can merit scholarships, which differ from school to school in their availability and criteria for application.

When federal, state, and institutional assistance programs fall short of covering the costs of your education, private student loans can help fill in the gap.