Refinancing your student loans is a great way to manage your student loans and take control of your finances. But when is the best time to refinance? If you’re looking to gain control of your student loans, then it might be time to refinance them.

How to Qualify for Student Loan Refinancing

Lenders look for a combination of indicators that show you are a reliable borrower. Since refinancing allows you to combine some or all your existing federal and/or private student loans into one new loan, you’ll need to qualify for the new loan. So, what do lenders look for when evaluating your application?

Here are a few of the requirements you’ll need to meet in order to qualify for a new loan.

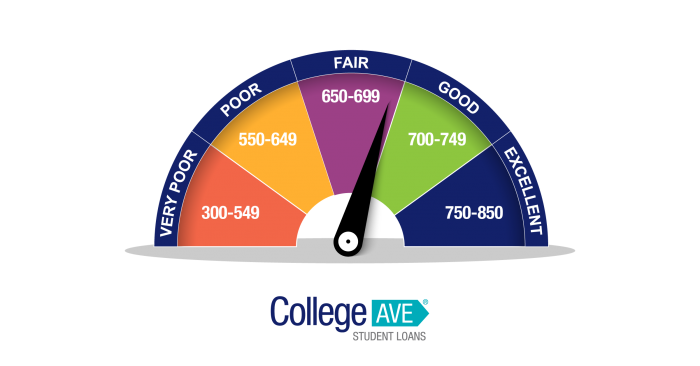

- Good Credit Score. Lenders will review your creditworthiness using your credit score. Your credit score is a calculation that indicates the likelihood that you’ll repay a loan in full and on time. If you have a lower credit score, you may have the option to add a cosigner in order to refinance your student loans.

- Strong Credit History. A meaningful part of your credit score is the length of your credit history. Lenders will want to make sure you have an established credit history over several years without late payments.

- Reasonable Debt-to-Income Ratio. You’ll need to demonstrate that you have a steady income that will enable you to pay off your debt. Lenders will evaluate this by calculating your debt-to-income ratio, which represents how much of your income is going directly to pay off any debt obligations. Calculate your debt-to-income ratio by dividing your monthly debt payments (including student loans, credit card payments, mortgages, car payments, etc.) by your gross monthly income.

Check out the College Ave Refinancing Pre Qualification Tool

The Best Time to Refinance Your Student Loans

Refinancing student loans can be done through banks, credit unions, and online private lenders. If you’re wondering exactly when to refinance student loans, keep in mind that, the goal is often to secure a lower interest rate, pay less each month, or to simplify your life by reducing the number of monthly payments you need to keep track of. But refinancing isn’t right for everyone. Should you choose to refinance your student loans, be sure to research your options. If you do decide to refinance your student loans, you’ll want to make sure that you’re in a good position to repay your new loan responsibly.

Here are a few tell-tale signs that it might be time to refinance your student loans.

- Multiple Student Loans. Many students graduate from college with a combination of federal and private student loans. You can refinance some or all your private and/or federal student loans into a new private student loans. This means you will have fewer student loan payments to remember each month – you could even end up with only one.

- High-Interest Rates. If you’ve established and maintained good credit, there are many reasons why you might qualify for a lower interest rate on a refi loan than you’re paying on your student loans today. If you are interested in getting a lower interest rate, it might be time to refinance and lock it in.

- Cosigner Release. Once you’ve had a chance to start paying back student loans, using credit cards responsibly, and successfully managing a car loan or mortgage, you’ll typically have a stronger credit history and a higher credit score. If you have a cosigner on one or more of your existing private loans, you may now qualify to take those loans on by yourself. Refinancing student loans in your name only will remove your cosigner’s obligation on your existing loans.

Refinancing While Still in School

You likely won’t be eligible to refinance your student loans while you’re still in school. Most students wait until after graduation to consider refinancing. It gives you a chance to establish and build income and credit. However, you can get a head start by building credit while you’re still in school. You can do this by responsibly making payments on your student loans. The best thing you can do with your loans while you’re still in school is to only take out as much as you need and start paying them off as soon as possible.

Market Factors

Private lenders like College Ave offer the choice of fixed or variable interest rates. Fixed interest rates will stay the same for the duration of your loan. Variable interest rates fluctuate with the market index, meaning they go up and down to adjust to banks’ lending practices. Lenders use a benchmark index rate to set their interest percentages. Many lenders use the London Interbank Offered Rate (LIBOR) as their benchmark, which was the standard interest rate banks pay when lending money to each other. With LIBOR retiring in 2023, most lenders – including College Ave – will start to use a new index called SOFR, short for Secured Overnight Financing Rate. SOFR is a broad measure of the cost of borrowing cash overnight collateralized by Treasury securities and a more reliable index than LIBOR.

This rate moves up and down according to the market, so the best time to refinance is when it’s lower. You can choose a fixed rate to lock in a consistent rate or choose a variable rate to take advantage of the fluctuations.

When to Consolidate Student Loans

Consolidation is a type of refinancing. Consolidation combines two or more loans into one loan, and in the process, the rate or terms usually change. You don’t have to consolidate in order to refinance with a private lender though; you could refinance a single loan to lower the interest rate or change the terms of that single loan. With College Ave Refi, you can choose to refinance only one loan or have the option to consolidate and refinance multiple loans.

Federal loans only can also be consolidated with a Direct Consolidation Loan through the federal government. Consolidation allows you to combine (or consolidate) all your federal student loans while maintaining their repayment terms. With a Direct Consolidation Loan, the interest rate is a weighted average of the interest rates on your existing federal student loans rounded up to the nearest one-eighth percent. Be sure to review your existing federal loans to make sure that they are eligible for consolidation.

How long does it take to refinance student loans?

Depending on the lender you choose, timeframes will vary. With College Ave, you can pre-qualify to confirm eligibility and get your personal rates, and use the Refinancing Calculator to see how much money you can save before your apply.

When you apply for a refi loan, you may be asked to provide proof of identity and/or proof of income depending on your application information. In that case, you’ll want to have your Social Security card or other ID handy as well as pay stubs or tax returns.

If you meet the qualifications for refinancing, getting started doesn’t take much time at all. At College Ave, our online application takes just three minutes.

Reasons Not to Refinance Your Student Loans

You’ve most likely been made aware of the various benefits that refinancing your student loan can offer, including the simplified payments, the potential to save a greater amount of money by paying less interest, or giving you a better payment timeline for your individual needs. However, it’s important to acknowledge that there are some drawbacks to refinancing. It’s important to evaluate the benefits of both private and federal student loans.

- Forfeit Federal Benefits. If you have federal student loans, taking out a private student loan to pay off your federal loans will cause you to lose benefits such as income-driven repayment plans, public service loan forgiveness, and possibly deferment and forbearance options.

- Pay More Interest Over Time. If you’re refinancing your loans and choose a longer repayment term to lower your monthly payment, you could end up paying more in interest over the life of the loan. It’s important to understand the terms of your existing student loans so that you choose the best option for you.

Weigh the Pros and Cons

Refinancing can make managing your student loans easier, but it’s important to make sure that you meet the requirements, understand how refinancing will affect your loans and choose the option that works best for your budget. When you’re ready, College Ave Student Loans offers student loan refinancing with low fixed and variable interest rates, so do your research to ensure that you’re making the best choice for you.

Updated as of 12/01/2021.