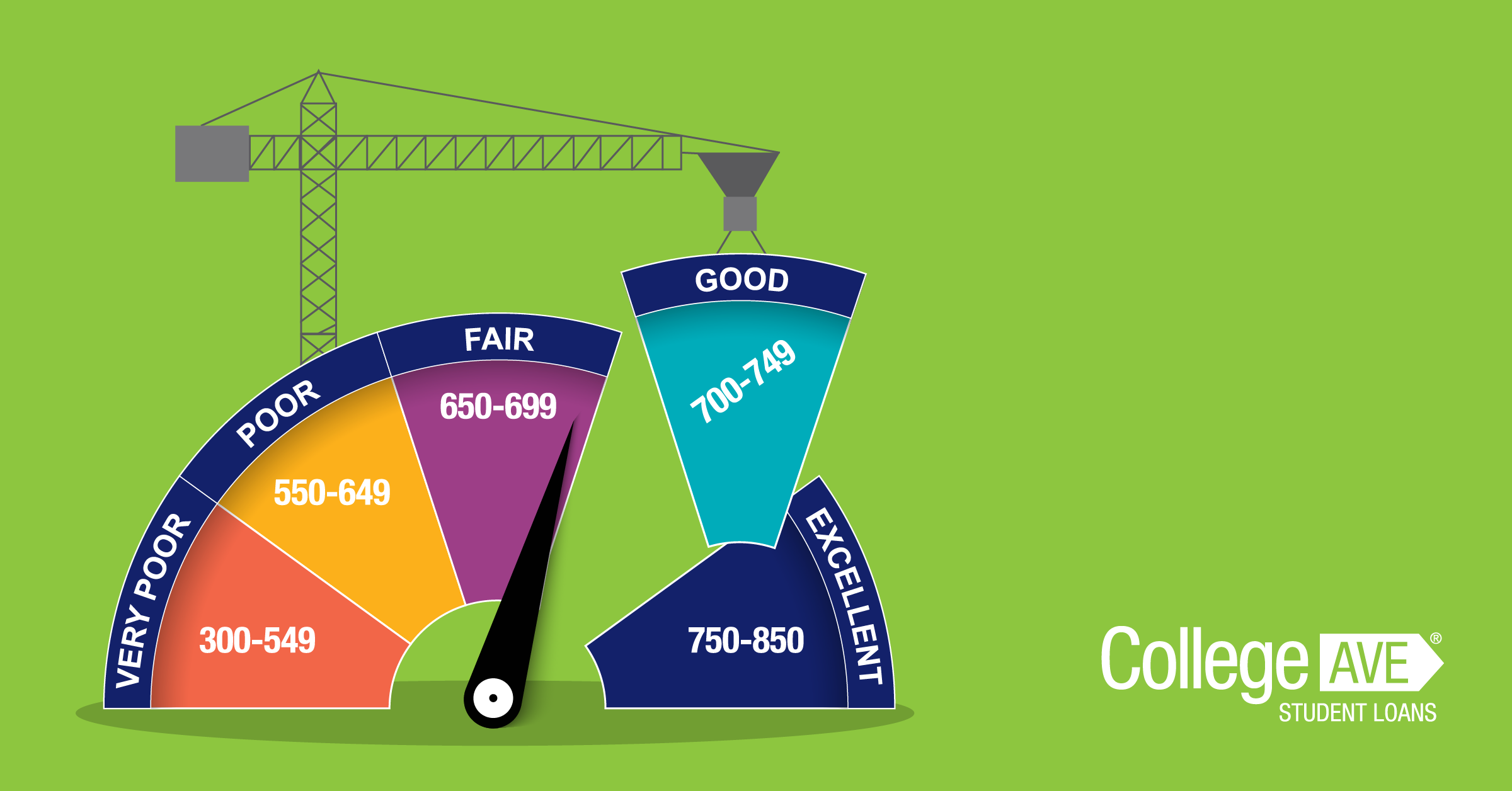

Credit plays a major role in your financial well-being. Your credit score helps you qualify for student loans, car loans, credit cards, apartments, and mortgages, among other things.

But it may be difficult to know how to establish or build credit for the first time, especially if you’re just starting out on your own. You might have no credit history, or thin credit, meaning you don’t have enough history to get a credit score.

There are a few ways for you to establish a credit history and help launch you on the road to financial independence. Here are our best tips for starting to build credit:

5 Ways to Start Building Credit for the First Time

1. Get a secured credit card

If you’re starting to build your credit score from scratch, a good place to start is with a secured credit card. A secured credit card is a type of credit card backed by an upfront cash deposit from the cardholder. This deposit amount is also the same as your credit limit. This ensures that you will have enough money to pay the lender back for your expenses. This is a great way to start building credit at 18, but it is not meant to be used forever. You’ll get the deposit back when you close the account and move on to a traditional credit card.

2. Become an authorized user on a credit card

If a friend, parent, or other guardian is willing to do so, they could add you as an authorized user on their credit card for you to start building credit. As an authorized user, that card’s payment history (good or bad) will show on your credit file. You’ll want to come to an agreement with the primary cardholder on how you’ll use the card before you’re added as an authorized user.

3. Take out a credit-builder loan

Credit-builder or secured loans are exactly what they sound like – they are designed to help people who have little or no credit history build credit. You will need to demonstrate to the lender that you have the income to make regular, on-time payments. Typically, the money you borrow is held by the lender in an account and is not released to you until the loan is repaid. Many local banks and credit unions offer this type of loan.

4. Get a loan with a cosigner

Like becoming an authorized user, getting a loan with a cosigner can help you build credit for the first time. If you have a student loan with a cosigner, both you and the cosigner are held equally responsible for making timely monthly payments. Late or missed payments could negatively impact your credit as well as the cosigner’s, so be sure to stay on top of your monthly budget.

5. Get credit for the bills you pay

There are some rent-reporting services that include your rent payments on your credit report – such as Rent Reporters or Rental Kharma. These services help build a positive history of on-time payments – and payment history accounts for 35% of your credit score. There are even some ways to have your cell phone and utility bills included on your credit reports as well. It’s important to know that on-time payments are essential to positively building your credit history. Late or missed payments could negatively impact your credit score.

Building Credit Do’s & Don’ts

Building a good credit score takes time and patience. Here are a few things you should get in the habit of doing to ensure you’re positively impacting your credit score:

- DO Make payments on time. Paying your bills on time, every time, is the best way to build your credit score. You should at least pay the minimum amount due, but if you can pay more than the minimum or pay the bill in full, that is the most helpful for your credit.

- DO Keep your credit balance low. Credit utilization – or how much of your total credit limit you’re using – is a key component of your credit score. A high utilization rate could indicate to financial institutions that you’re having a hard time paying your bills on time. A utilization rate of 30% or less is ideal for building good credit.

- DO Check your credit report for errors. You are eligible to receive a free credit report from each of the 3 reporting agencies – Experian, Equifax, and TransUnion – every year. It’s important to check your annual reports and correct any errors you might find.

- DON’T Close a credit card account. Surprisingly, closing a credit card account can hurt your credit score. Your credit score takes into account how long you’ve had an account (or the average age of all of your credit accounts). Closing an account can lower your average, which could negatively impact your credit score. Unless you have a good reason to close your account (like high annual fees or interest rates), you should consider keeping it open.

- DON’T Stray from your budget. Making a budget, and actually sticking to it, can help you avoid overspending and taking on debts you may not be able to pay back easily. Smart decisions about what you can and can’t afford will go a long way in building and maintaining good credit.

Building your credit profile, especially when you’re young, can be tricky, but it’s not impossible! With a little patience and preparation, you can take steps now to begin establishing a good credit history and score.